Why do finance teams still deal with repeated revisions, even when the people and systems are already in place?

For most organizations, the issue is not capability. It is clarity. Work moves through the process, gets reviewed, and comes back with comments. Adjustments are made, then reviewed again. This loop becomes embedded in the workflow, especially in areas like reconciliations, reporting, and audit preparation.

Over time, leaders begin to accept this as part of operations. They build buffers into timelines. They allocate additional review layers. They assume that rework is unavoidable. But evidence across industries shows a different pattern.

Rework is not random. It is typically driven by unclear requirements, inconsistent execution standards, and incomplete inputs. In outsourcing environments, where work moves across organizational boundaries, these issues become more visible and more expensive.

Key Takeaways

- Rework is primarily driven by unclear standards rather than a lack of capability

- A Definition of Done creates a shared, enforceable standard for completion

- It improves alignment between internal teams and outsourcing partners

- Clear standards lead to faster delivery and fewer revisions

- Over time, it supports scalability, control, and better decision-making

The Definition of Done addresses this at its source. It creates a shared, enforceable

standard for what “complete” means, reducing ambiguity before it turns into rework.

What “Definition of Done” Looks Like in Finance Operations

The Definition of Done (DoD) is widely used in Agile environments to ensure that work is not only finished, but validated and ready for use. In finance and accounting outsourcing, the concept becomes even more practical. It answers a critical operational question:

when can this work move forward without coming back?

Instead of relying on individual judgment, the DoD establishes a consistent structure that every task must meet before it is considered complete. That could apply to:

- Monthly reconciliations

- Close schedules

- Management reports

- AP/AR deliverables

- Tax-ready workpapers

- Audit support files

- Outsourced bookkeeping outputs

At a practical level, this structure rests on four elements:

- Inputs are complete and validated

The work does not begin until all required data, documents, and scope parameters are clearly defined. This prevents downstream corrections caused by missing or inconsistent information (e.g., Bank statements received, Trial balance finalized, Source reports extracted, and Deadlines confirmed)

- Execution follows a defined process

The steps are standardized, reducing variability between team members and ensuring that outcomes are consistent regardless of who performs the work

(e.g., Reconciliation format is standardized, Review checklist is consistent, Journal entries follow approval logic, and Close steps are sequenced clearly)

- Outputs are supported by clear evidence

Every figure is traceable, every adjustment is explained, and supporting documentation is complete. This reduces questions during review and strengthens audit readiness

(e.g., Supporting schedules attached, Variances explained, Adjustments documented, and Source references included)

- Review criteria are explicit

Approval is based on predefined standards, not individual interpretation. This eliminates subjective feedback and shortens review cycles

(e.g., Supporting schedules attached, Variances explained, Adjustments documented, Source references included)

When these elements are applied consistently, “done” becomes measurable rather than assumed. Teams know exactly what is required before work moves forward, and leaders gain confidence that outputs meet expectations without repeated clarification.

Why Rework Persists in Finance and Outsourcing

Rework is often treated as a performance issue, but in most cases, it is a structural one.

Research on project delivery

and operational workflows consistently identifies the same root causes. Rework tends to originate from unclear scope, communication gaps, and a lack of standardization. These are upstream issues, not execution failures.

How DoD Strengthens Outsourcing Performance

Outsourcing introduces complexity, but it also introduces an opportunity to formalize standards. A

Definition of Done provides the structure needed to align internal teams and external partners around a single operating model. It translates expectations into something that can be consistently executed and objectively measured. This shift has several important implications.

First, it reduces dependency on continuous clarification. When expectations are defined upfront, teams spend less time resolving misunderstandings after the fact. Second, it improves accountability. Deliverables can be assessed against clear criteria, making performance discussions more objective and less subjective.

Third, it stabilizes delivery. When both sides follow the same standard, outputs become more predictable, even as volumes increase or team composition changes. Over time, this changes the nature of the outsourcing relationship. Instead of managing exceptions, leaders can focus on managing performance.

The difference is subtle but significant. The conversation moves from “what went wrong” to “how do we improve further.”

The Business Impact: Where Firms See Real Gains

For decision-makers, the value of a Definition of Done is not theoretical. It shows up in measurable operational improvements. The most immediate impact is the reduction of rework. When expectations are clear before execution begins, the need for revisions decreases. This directly improves cycle times and frees up capacity across the team.

Quality also improves more consistently. Because outputs must meet defined evidence and review standards, issues are identified earlier in the process. This reduces the risk of errors reaching later stages, where they are more costly to correct.

There is also a significant impact on scalability. As firms grow or expand their use of outsourcing, maintaining consistency becomes more challenging. A well-defined standard ensures that outputs remain uniform, even as work is distributed across multiple teams.

From a leadership standpoint, the benefits become clear in day-to-day operations:

- Stronger first-pass accuracy, reducing review cycles

- Faster close timelines, with fewer bottlenecks

- More reliable outputs, supporting better decision-making

These improvements do not just enhance efficiency. They strengthen the overall control environment.

A Practical Finance Scenario: Before and After

Consider a monthly close process supported by an

outsourced team. Without a clear Definition of Done, the offshore team submits schedules that appear complete but lack sufficient supporting detail. The internal team reviews the work, identifies gaps, and sends it back. Each revision cycle delays the close and increases pressure on both teams.

With a defined standard, the process changes from the start. Inputs are validated before work begins, ensuring that the data is complete. The execution follows a consistent structure, reducing variability. Outputs include all required supporting documentation, clearly tied to source data.

Review criteria are applied consistently, minimizing subjective feedback. The result is not just fewer revisions. It is a smoother, more predictable close process. For finance leaders, this predictability is critical. It allows for better planning, more accurate forecasting, and reduced operational stress during peak periods.

Why This Becomes the Foundation for Standardization

Standardization

is often positioned to improve efficiency, but its deeper value lies in control and scalability.

A Definition of Done operationalizes standardization. It turns expectations into something observable and repeatable, which is essential in environments where work is distributed across teams and locations.

It also aligns with broader operational frameworks. Lean principles emphasize the elimination of non-value-added activities, and rework is one of the most common forms of waste. Vendor management frameworks highlight the importance of clearly defined deliverables and measurable outcomes.

By defining what “done” looks like, organizations reduce variability and create a stable foundation for growth.

For finance leaders, this is particularly important. As organizations scale, complexity increases. Without clear standards, that complexity translates into inconsistency. With the right standards in place, it becomes manageable.

Creating a Definition of Done in Finance & Accounting Outsourcing

A Definition of Done is not a template or checklist. It is an operational agreement that reflects how financial work is executed, reviewed, and approved. According to

Atlassian, a DoD is a shared set of criteria that determines when work is complete and ready for use, and it should be collaboratively defined and continuously improved.

For finance leaders, this principle is critical. If “done” is not defined jointly between internal teams and outsourcing partners, misalignment becomes embedded in the workflow. A structured approach typically includes five steps.

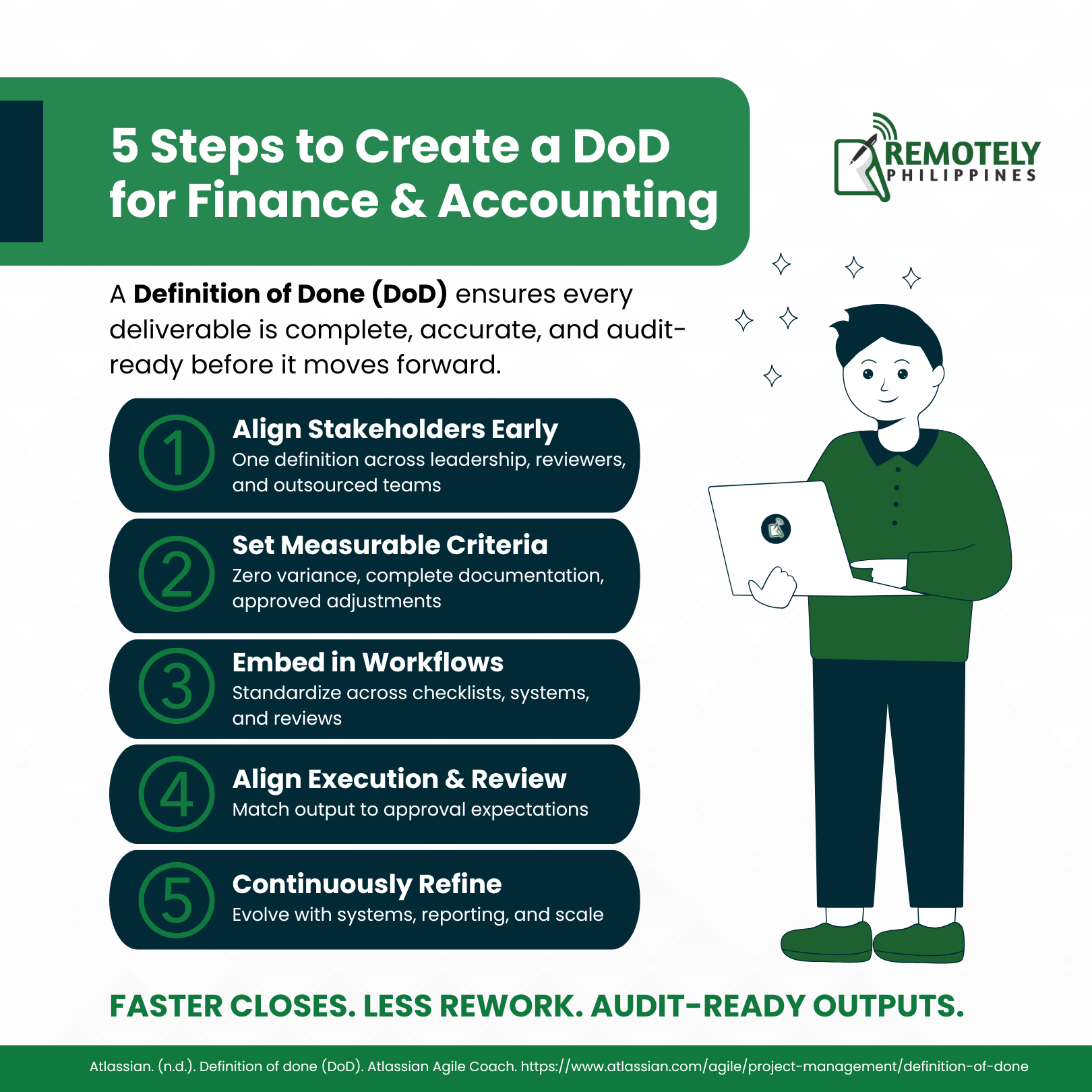

1. Align the Right Stakeholders Early

A Definition of Done cannot be defined in isolation. It must involve:

- Internal finance leadership

- Controllers or reviewers

- Outsourced delivery leads

- Compliance or audit stakeholders, where relevant

The goal is alignment of expectations before execution begins. Without this, each group operates with its own interpretation of completeness, which surfaces later as rework.

2. Define Clear, Measurable Completion Criteria

This is where most DoDs fail. Completion criteria must be specific enough to eliminate interpretation. Vague terms like “reviewed” or “finalized” are not operational standards. Stronger criteria include:

- Reconciliation matches source systems with zero unexplained variance

- Supporting documentation is complete, attached, and traceable

- Adjustments are clearly documented and approved

The criteria should be specific, relevant, and aligned with stakeholder expectations rather than internal assumptions. In finance, those stakeholders often include leadership, auditors, and regulators.

3. Translate Criteria into Operational Checkpoints

A Definition of Done only becomes effective when embedded into workflows. This includes integrating standards into:

- Close checklists

- Task management systems

- Review templates

The objective is consistency. Every deliverable follows the same validation path before it is considered complete. Without this operational layer, even well-defined standards remain theoretical.

4. Align Execution Standards with Review Expectations

One of the most common breakdowns in finance operations occurs between execution and review. A strong DoD should clearly define:

- What qualifies for review

- What triggers rejection or revision

- What level of supporting evidence is required

When review standards are not aligned with execution criteria, teams operate under different definitions of quality. This is one of the primary drivers of repeated rework cycles in finance and outsourcing environments.

5. Treat It as a Living Operational Standard

A Definition of Done is not static. As systems evolve, reporting requirements change, and business models shift, the definition must be revisited. The teams should regularly refine their DoD to improve quality and prevent recurring issues over time. For finance leaders, this reframes it as a governance tool that evolves with the organization rather than a fixed procedural document.

FAQs

Why This Matters for Finance Leaders

At a

strategic level, the Definition of Done changes how finance operations are managed. It shifts focus from correction to prevention. Instead of relying on review cycles to identify issues, quality is built into the process from the start.

This creates three measurable outcomes:

- More predictable outcomes across recurring finance deliverables

- Reduced cycle times in recurring finance processes

- Greater consistency across internal and outsourced teams

More importantly, it reduces dependency on individual interpretation and replaces it with standardized execution logic. For organizations leveraging outsourcing, this becomes essential for scaling without losing control over quality.

Conclusion

Rework in finance and accounting outsourcing is often accepted as inevitable, but it is usually a symptom of missing operational clarity. The Definition of Done resolves this by establishing a shared, measurable standard for completion that applies across both internal and external teams.

It ensures that work is not only completed but completed in a way that is consistent, verifiable, and aligned with stakeholder expectations. In practice, this shifts finance operations from reactive correction to proactive control. It also strengthens governance by making expectations explicit and measurable, allowing leaders to manage performance with greater precision.

More importantly, it enables scalability. As organizations grow and outsourcing expands, variability naturally increases. A well-defined standard of completion ensures that this variability does not translate into inconsistency or risk. For finance leaders, the implication is clear. The effectiveness of your operations is not only determined by your people or systems, but by how precisely “done” is defined—and how consistently it is applied.